About Our Depreciation Rate Calculator

At the point, when your business purchases a resource (an actual property claimed by your organisation), you can deduct the expense of that resource as a cost of doing business. Notwithstanding, charge guidelines say you should spread the payment of that resource over its valuable assessed life. That sort of long haul derivation is called devaluation.

Deterioration is characterised as the worth of a business resource over its useful life. How deterioration is determined decides the amount of a devaluation derivation you can take in any year. So it's essential to comprehend the strategies for computing devaluation.

- The depreciation method is a way to spread out the cost of a long-term business asset over several years.

- The fundamental way to calculate depreciation is to take the asset's price minus any salvage value over its useful life.

- For accounting and tax purposes, depreciation is calculated differently, but the basic idea remains the same.

- The deduction of depreciation expenses every year can reduce your tax bill as a small business owner.

Don’t worry, our depreciation rate calculator is here to help you out with the easy calculation in seconds.

What Kind of Assets Can You Depreciate?

There are many types of assets you can consider in the depreciation list.

- You own it.

- You use it in your business and produce income.

- Determine its helpful life.

Here are some examples of assets depreciated includes:

- Vehicles

- Machines Equipment

- House Interiors

- Digital Equipment

What is an Asset?

- A resource is anything with dollar esteem. The IRS additionally alludes to resources as "property." It can be either substantial or immaterial.

- An unmistakable resource can be contacted—think the place of business, conveyance truck, or PC.

- A theoretical resource can't be contacted—yet it can, in any case, be traded. Models incorporate a patent, copyright, or other protected innovation.

- Both substantial and theoretical resources can be devalued. On account of elusive resources, the demonstration of devaluation is called amortisation.

What Are the Most Important Types of Depreciation Methods?

Depreciation is a recurring expense, and various formulas determine the book value of an asset. Depreciation is commonly calculated by:

- Straight-line

- Double declining balance

- Units of production

- Sum of years digits

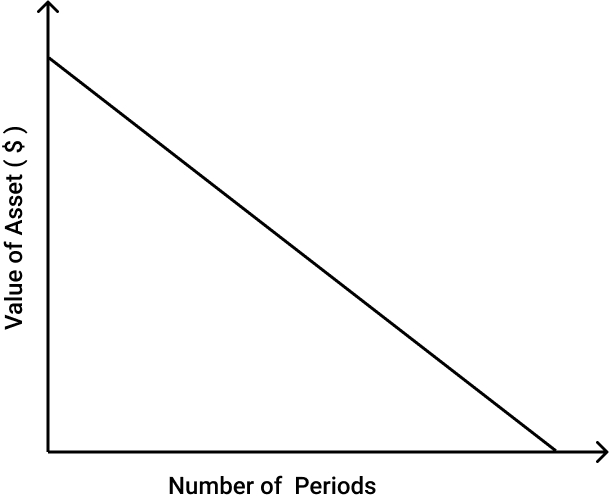

1.Straight Line Depreciation

Straight-line deterioration is a basic technique for computing how much a specific fixed resource devalues (loses esteem) after some time.

The straight-line technique for deterioration expects a steady pace of devaluation. It computes how much a particular resource deteriorates in one year and afterwards devalues the resource by that sum consistently later.

If you envision straight-line deterioration, it would resemble this:

Asset's straight-line depreciation formula includes:

Here,

- Cost of the asset: asset's original purchase price

- Salvage value: asset's real value during the useful life

- The useful life of the asset: Measures the expected lifetime of an asset by the company

As an example, here is how to calculate straight-line depreciation:

With our straight line depreciation calculator, you can easily calculate straight line depreciation.

2.Double Declining Balance

Dual Declining Balance Method is one of the sped-up techniques utilised for the estimation of the deterioration add up to be charged in the pay articulation of the organisation, and it is determined by increasing the Book worth of resource with Rate of devaluation according to straight-line strategy and 2.

Double Declining Balance Depreciation Method

- A double-declining balance strategy is a sped-up devaluation technique wherein the resource esteem deteriorates double the rate done in the straight-line technique. Since the devaluation is done at a quicker rate (two times to be exact) of the straight-line strategy, it is called sped up deterioration.

- Nonetheless, sped up devaluation doesn't imply that the deterioration cost will likewise be higher. The resource will deteriorate by a similar sum; as it may, it will be discounted higher in the early long periods of its valuable life. The devaluation cost will be lower later when contrasted with the straight-line strategy for deterioration.

Double Declining Balance Method Formula

The depreciation amount will be as follows:

- Formula for the double declining balance method is = 2 X Cost of the asset & Depreciation rate.

- Balance Formula with Double Declining = 2 X Cost of the asset/Useful Life

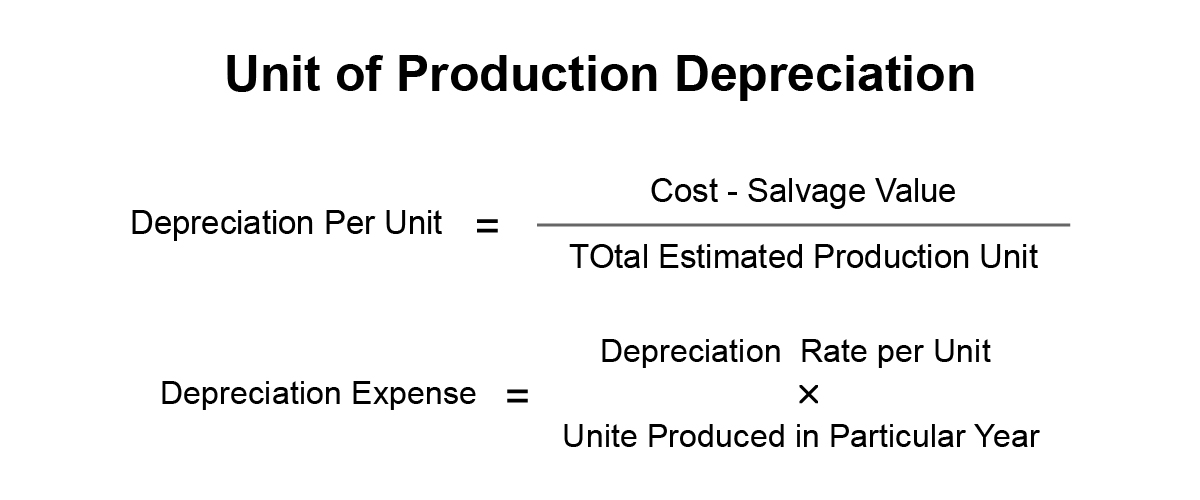

3.Units of production

An asset's depreciation over time is calculated using the unit of production method. Simply, This method of depreciation charges assets according to units of production.

Unit of Production Depreciation Formula

To understand the unit of production depreciation formula better, we will break it down into two parts.

Step 1: per unit depreciation formula has given below,

Depreciation per Unit = ( Cost- Salvage Value) / Total Estimated Production Unit.

Step 2: The expense formula of depreciation is given below,

Depreciation Expense = Depreciation Rate per Unit × Unit Produced in a Particular Year.

Cost: It incorporates bought value, establishment, conveyance charge, accidental costs.

Salvage Value: the worth will get toward the finish of the existence of a resource.

Estimated Unit of Production: It is fundamentally an assessment of the unit delivered by the resource over its valuable life.

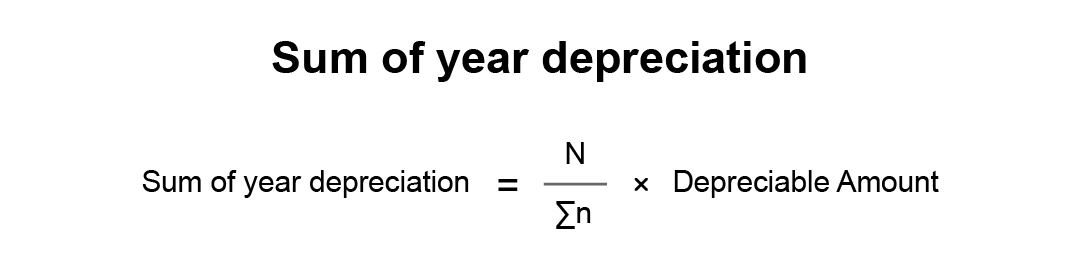

4.Sum of Years Digits

We can calculate the accelerated depreciation by the sum of years digits method using this method.

Formula:

The given procedure calculates depreciation expense under the digits method of "The Sum of Years."

N = Valuable life of the asset

∑n = Sum of Years

Depreciable Amount = Total Acquisition Cost – Salvage Value

How Does Depreciation Term Work?

At the point, when your business purchases property for long haul use, you can take derivations for the expense of the property by spreading it for more than quite a while utilising an interaction called devaluation. The Internal Revenue Service (IRS) calls this kind of property (like vehicles, apparatus, hardware, and furniture) capital resources.

Suppose you bought a piece of PC gear for your business at the expense of $8,000. The normal PC keeps going 10 years, so it diminishes in esteem by 10% every year. You can take a derivation for deterioration of $800 every year on your business government form.

The Most Effective Method to Calculate Depreciation

To work out deterioration, you want to know:

- The expense of the (resource premise), including costs for purchasing the resource, delivery, arrangement, and preparing

- The helpful existence of the resource (likewise called the recuperation time frame)

- The rescue esteem toward the finish of its valuable life

You can track down the helpful life (called "recuperation period" for charge motivations behind) explicit business resources in Publication 946 How to Depreciate Property.

Devaluation is determined every year for charge purposes. The most widely recognized devaluation is straight-line deterioration, taking a similar measure of deterioration every extended period of the resource's valuable life.

For instance, the primary year estimation for a resource that costs $15,000 with a rescue worth of $1,000 and a helpful existence of 10 years would be $15,000 less $1,000 isolated by 10 years rises to $1,400.

The resource should be put in help (set up and utilised) in the primary year that devaluation is determined.